Management's Discussion

and Analysis

Financial Statements

and Notes

1303 East Algonquin Road

Schaumburg, Illinois 60196

March

Rosemont Theater

5400 N. River Road

Rosemont, Illinois 60018

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registrantý | ||

| Filed by a Party other than the Registranto | ||

Check the appropriate box: | ||

| o | Preliminary Proxy Statement | |

| o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ý | Definitive Proxy Statement | |

| o | Definitive Additional Materials | |

| o | Soliciting Material Pursuant to §240.14a-12 | |

MOTOROLA, INC. | ||||

(Name of Registrant as Specified In Its Charter) | ||||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

| ý | No fee required | |||

| o | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11 | |||

| (1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

| o | Fee paid previously with preliminary materials. | |||

| o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

| ||

| Proxy Statement | ||

Management's Discussion and Analysis | ||

Financial Statements and Notes | ||

| PRINCIPAL EXECUTIVE OFFICES: 1303 East Algonquin Road Schaumburg, Illinois 60196 March | PLACE OF MEETING: Rosemont Theater 5400 N. River Road Rosemont, Illinois 60018 | |

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

To the Stockholders:

Our Annual Meeting will be held at the Rosemont Theater, 5400 N. River Road, Rosemont, Illinois 60018 on Monday, May 6, 20025, 2003 at 5:00 P.M., local time.

The purpose of the meeting is to:

Only Motorola stockholders of record at the close of business on March 15, 200214, 2003 will be entitled to vote at the meeting. Please vote in one of the following ways:

PLEASE NOTE THAT ATTENDANCE AT THE MEETING WILL BE LIMITED TO STOCKHOLDERS OF MOTOROLA AS OF THE RECORD DATE (OR THEIR AUTHORIZED REPRESENTATIVES) HOLDING ADMISSION TICKETS OR OTHER EVIDENCE OF OWNERSHIP. THE ADMISSION TICKET IS DETACHABLE FROM YOUR PROXY CARD. IF YOUR SHARES ARE HELD BY A BANK OR BROKER, PLEASE BRING TO THE MEETING YOUR BANK OR BROKER STATEMENT EVIDENCING YOUR BENEFICIAL OWNERSHIP OF MOTOROLA STOCK TO GAIN ADMISSION TO THE MEETING.

| By order of the Board of Directors, | ||

A. Peter Lawson Secretary |

Christopher B. GalvinChairman of the Board andChief Executive Officer

March 29, 200227, 2003

Dear Fellow Stockholders:

2001 was a tougher year than any other in the history of Motorola. Like others, we inopportunely chased the dot-com and telecom boom in 2000. We built-up manufacturing capacity and a global cost structure anticipating $45 billion in sales in 2001, having achieved $37.6 billion in sales in 2000. Unfortunately, given the severe downturn in telecom markets, dramatic fall off in semiconductor demand and horrific world events during 2001, our actual global sales were approximately $30 billion. Consequently, our major management focus was aggressively directed to reversing the impact of 2001 and returning to profitability.

We find our financial performance as unacceptable as our stockholders do. We've taken the tough, necessary steps to improve our cost structure, institute new efficiencies across the corporation and enhance our balance sheet. We enter 2002 as a leaner, more agile, more focused and more fiscally sound company. We intend to remain focused on our new course of action to enhance the shareholder value of this great company. I thank you for your continued support of Motorola through these trying times.

At the same time, weYou are committed to our key beliefs—uncompromising integrity and constant respect for people. Our company was built on these key beliefs and they fundamentally dictate the way we do business. We will continue to be transparent about our performance and we will continue to provide financial statements and other information that fully and accurately describe the condition of our company and the risks and opportunities that face our businesses.

You arecordially invited to attend the 2002Motorola's 2003 Annual Meeting of Stockholders to be held on Monday, May 6,5, 2003, in Rosemont, Illinois. I look forward to our Annual Meeting each year because it gives me a chance to report to you on our progress during the last year. In 2002, during the middle phase of our turnaround, we exceeded the vast majority of the financial metrics we set out to achieve. Most importantly, in the second half of 2002 we returned Motorola to profitability, even in the face of declining sales. Despite these achievements, we are not satisfied. I will report on the last phase of our turnaround at the meeting, as well as hear your questions and concerns.

In 2003, we are also celebrating an important landmark in Motorola's history—the 75th anniversary of our founding. In 1928, we incorporated with $565 in cash, $750 in tools and a design for our first product. Today, we enter our 75th year as a technology leader. We are helping to build a global society unimagined by our founders, guided by high ethics and principles and executing a forward-looking plan to help us outperform our competitors, generate profit and cash and drive growth.

At this year's Annual Meeting, in addition to electing the 13 members of our Board of Directors, we are asking our shareholders to consider two important proposals for our 2002 Annual Meeting. First, we are asking for your approval ofapprove the Motorola Omnibus Incentive Plan of 2002. The use of stock options and other stock awards to compensate employees remains widely prevalent among technology companies.2003. The Board has adopted the 20022003 Plan in order to maintain the flexibility we need to keep pace with our competitors and to effectively recruit, motivate and retain the caliber of employees essential for our company'sCompany's success. The 2002 Plan isuse of stock options and other stock awards to compensate employees remains integral to Motorola's compensation strategies and programs in 2002programs. Stock options and going forward.

Weother stock awards are also asking for your approvalissued to a wide range of an amendmentmanagerial and individual contributors throughout the Company and all over the world to encourage employees to further align their personal financial worth to the Company's share price growth. During 2002, more than 44,000 employees received Motorola Employee Stock Purchase Planstock options. This means our stock incentive plans are used to motivate almost half of 1999 to make 50 million additional shares available for purchase byour employees. The Employee Stock Purchase Plan continues to be an important tool in a very competitive employment market. It also encourages employees to own more shares of Motorola and thereby further aligns their interests with those of our stockholders.

Each of these proposalsproposal is discussed in greater detail in the enclosed Proxy Statement.

I encourage each of you to vote your shares through one of the three convenient methods described in the enclosed Proxy Statement. I would appreciate your support of these proposalsthe nominated directors and the proposal to approve the Motorola Omnibus Incentive Plan of 2003 and, as always, I thank you for your continued support of Motorola.

Very truly yours,

Christopher B. Galvin

Chairman of the Board

and Chief Executive Officer

TABLE OF CONTENTS

PROXY STATEMENT

| | PAGE | ||

|---|---|---|---|

| • Voting Procedures | 1 | ||

| • Who Can Vote | 1 | ||

| • How You Can Vote | 1 | ||

| • How You May Revoke Your Proxy or Change Your Vote | 1 | ||

| • General Information on Voting | 1 | ||

| • Voting by Participants in the Company's 401(k) Profit Sharing Plan | 2 | ||

• Proposal 1—Election of Directors for a One-Year Term | 3 | ||

| • Nominees | 3 | ||

| • Meetings of the Board of Directors of the Company | 6 | ||

| • Corporate Governance Initiatives | 6 | ||

| • Committees of the Board of Directors | |||

| • Director Compensation and Related Transactions | |||

• Proposal 2—Adoption of the Motorola Omnibus Incentive Plan of | |||

| • | |||

15 | |||

• Ownership of Securities | 17 | ||

• Executive Compensation | 19 | ||

| • Summary Compensation Table | 19 | ||

| • Stock Option Grants in | |||

| • Aggregated Option Exercises in | |||

| • Long-Term Incentive Plans—No Awards in | |||

| • Retirement Plans | 23 | ||

| • Employment Contracts, Termination of Employment and Change in Control Arrangements | |||

• Report of Compensation Committee on Executive Compensation | |||

• Report of Audit and Legal Committee | |||

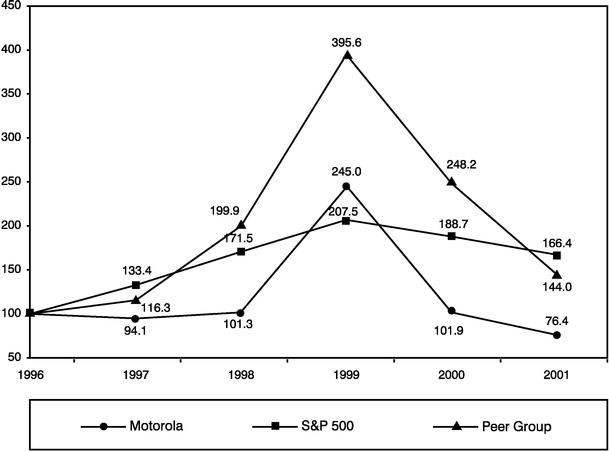

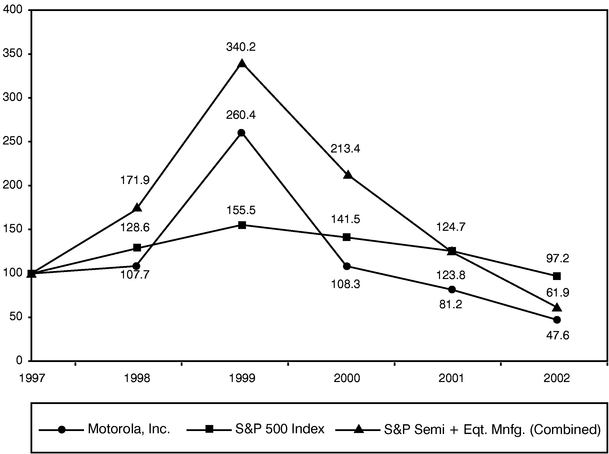

• Performance Graph | |||

• Other Matters | |||

• Appendix A: Audit and Legal Committee Charter | A-1 | ||

APPENDIX OF FINANCIAL INFORMATION | |||

• Management's Discussion and Analysis of Financial Condition and Results of Operations | F-1 | ||

• Financial Highlights | F-41 | ||

• Financial Statements and Notes | F-42 | ||

PROXY STATEMENT—VOTING PROCEDURES

The Board of Directors is soliciting proxies to be used at the May 6, 20025, 2003 Annual Meeting. Your vote is very important. This proxy statement, the form of proxy and the 20012002 Summary Annual Report will be mailed to stockholders on or about March 29, 2002.27, 2003. The Summary Annual Report is not a part of this proxy statement. The proxy statement and Summary Annual Report are also are available on the Company's website at www.motorola.com/investor.

Only stockholders of record at the close of business on March 15, 200214, 2003 (the "record date") will be entitled to notice of and to vote at the Annual Meeting or any adjournments thereof. On that date, there were 2,270,627,4342,315,606,622 issued and outstanding shares of the Company's common stock, $3 par value per share ("Common Stock"), the only class of voting securities of the Company.

This year thereThere are three convenient voting methods:

How You May Revoke Your Proxy or Change Your Vote

You can revoke your proxy at any time before it is voted at the 20022003 Annual Meeting by either:

No Cumulative Voting

You are entitled to cast one vote for each share of Common Stock you own on the record date. Stockholders do not have the right to vote cumulatively in electing directors.

Quorum Required

In order for business to be conducted, a quorum must be represented at the Annual Meeting. A quorum is a majority of the shares entitled to vote at the Annual Meeting. Shares represented by a proxy in which authority to vote for any matter considered is "withheld", a proxy marked "abstain" or a proxy as to which there is a "broker non-vote" will be considered present at the meeting for purposes of determining a quorum.

Required Vote to Elect Directors

Directors will be elected by a plurality of the votes cast at the Annual Meeting, meaning the 13 nominees receiving the most votes will be elected. Only votes cast for a nominee will be counted. Unless indicated otherwise by your proxy, the shares will be voted for the 13 nominees named in this proxy statement. Instructions on the accompanying proxy to withhold authority to vote for one or more of the nominees will result in those nominees receiving fewer votes but will not count as a vote against the nominees.

Required VotesVote to Pass Other ProposalsAdopt the Motorola Omnibus Incentive Plan of 2003

In order to (i) adopt the Motorola Omnibus Incentive Plan of 2002, (ii) authorize the amendment to the Motorola Employee Stock Purchase Plan of 1999, or (iii) recommend that the Board consider adoption of any shareholder proposal,2003, an affirmative vote of a majority of the shares present in person or by proxy and entitled to vote at the Annual Meeting is required. For each of these proposals,this proposal, an abstention will have the same effect as a vote against the proposal. Broker non-votes will not be voted for or against any of these proposalsthis proposal and will have no effect on any of these proposals.this proposal.

Other Information

If you are the beneficial owner of shares held in "street name" by a broker, the broker, as the record holder of the shares, is required to vote those shares in accordance with your instructions. If you do not give instructions to the broker, the broker will be entitled to vote the shares with respect to "discretionary" items but will not be permitted to vote the shares with respect to "non-discretionary" items

PROXY STATEMENT 1

(those shares are treated as "broker non-votes"). The election of directors and all other proposals in this proxy statement are "discretionary" items.

All shares that have been properly voted—whether by telephone, Internet or mail—and not revoked will be voted at the Annual Meeting in accordance with your instructions. If you sign your proxy card but do not give voting instructions, the shares represented by that proxy will be voted as recommended by the Board of Directors.

If any other matters are properly presented at the Annual Meeting for consideration, the persons named as proxies in the enclosed proxy card will have the discretion to vote on those matters for you. At the date we filed this proxy statement with the Securities and Exchange Commission, the Board of Directors did not know of any other matter to be raised at the Annual Meeting.

Voting by Participants in the Company's 401(k) Profit Sharing Plan

If a stockholder is a participant inowns shares of Common Stock through the Motorola 401(k) Profit Sharing Plan (the "401(k) Plan"), the proxy card also will serve as a voting instruction for the trustees of that plan where all accounts are registered in the same name. If shares of Common Stock in the 401(k) Plan are not voted either by telephone, via the Internet, or by returning the proxy card representing such shares, those shares will be voted by the trustees in the same proportion as the shares properly voted by other participants owning shares of Common Stock in the 401(k) Plan.

2 PROXY STATEMENT

PROPOSAL 1

ELECTION OF DIRECTORS FOR A ONE-YEAR TERM

The term of office of all present directors of the Company will expire on the day of the 20022003 Annual Meeting upon the election of their successors. The number of directors of the Company to be elected at the 20022003 Annual Meeting is 13. The directors elected at the 20022003 Annual Meeting will serve until their respective successors are elected and qualified or until their earlier death or resignation.

Each of the nominees named below except for Mr. Warner, is currently a director of the Company and each was elected at the Annual Meeting of stockholders held on May 7, 2001,6, 2002, except for Mr. BreenMs. Nooyi and Mr. WarnerZafirovski who are standing for election for the first time. Robert L. GrowneyAnne P. Jones is retiring from the Board and Ronnie C. Chan arewill not be standing for re-electionre-election. Ms. Jones is expected to enter into a consulting agreement with the Board.Company following her retirement. The ages shown areconsulting arrangement will enable the Board and the Company to continue to benefit from Ms. Jones knowledge of the Company and expertise as of December 31, 2001.the need arises.

If any of the nominees named below is not available to serve as a director at the time of the 20022003 Annual Meeting (an event which the Board does not now anticipate), the proxies will be voted for the election as director of such other person or persons as the Board may designate, unless the Board, in its discretion, reduces the number of directors. The ages shown are as of December 31, 2002.

| CHRISTOPHER B. GALVIN, Principal Occupation: Chairman of the Board and Chief Executive Officer, Motorola, Inc. Director since 1988 Age— Mr. Galvin began working for the Company in 1967 and he served in sales, sales management, marketing, product management, service management and general management positions in the Company's various businesses. He served as President and Chief Operating Officer from 1993 until he became Chief Executive Officer on January 1, 1997. In June 1999, Mr. Galvin became Chairman of the Board. Mr. Galvin received a bachelor's degree from Northwestern University and a master's degree from the Kellogg Graduate School of Management at Northwestern University. | |

| ||

| FRANCESCO CAIO, Principal Occupation: Chief Executive Officer, Netscalibur Director since 2000 Age— Mr. Caio is the Chief Executive Officer of Netscalibur, a pan-European IP services provider. Mr. Caio is also a member of the Board of Merloni Elettrodomestici, where he was Chief Executive Officer from 1997 to 2000. Merloni Elettrodomestici is the third-largest manufacturer of domestic appliances in Europe. Mr. Caio obtained his Masters degree in Computer Science from the Politecnico di Milano and his MBA as a Luca Braito Scholar from INSEAD at Fountainbleau, France. Mr. Caio is a citizen of Italy. | |

PROXY STATEMENT 3

| H. LAURANCE FULLER, Principal Occupation: Retired; Formerly Co-Chairman of the Board, BP Amoco, p.l.c. Director since 1994 Age— Mr. Fuller retired as Co-Chairman of BP Amoco, p.l.c., an energy company, in March 2000. Prior to holding that position, he had served as Chairman and Chief Executive Officer of Amoco Corporation since 1991. He is also a director of Abbott Laboratories, J.P. Morgan Chase & Co. and | |

| ||

PROXY STATEMENT 3

| JUDY C. LEWENT, Principal Occupation: Executive Vice President and Chief Financial Officer and President, Human Health Asia, Merck & Co., Inc. Director since 1995 Age— Ms. Lewent has been Executive Vice President | |

| DR. WALTER E. MASSEY, Principal Occupation: President of Morehouse College Director since 1993 Age— Dr. Massey has been President of Morehouse College since 1995. In 1991, he was appointed by President Bush as the Director of the National Science Foundation after which he was Provost and Senior Vice President for the University of California System. Prior to that he had been director of the Argonne National Laboratory and vice president for research at the University of Chicago. Dr. Massey received a Ph.D. degree in Physics and a Master of Arts degree from Washington University. He also holds a Bachelor of Science degree in Physics and Mathematics from Morehouse College. He is a director of BP Amoco, p.l.c., BankAmerica Corporation and McDonalds, Inc. Dr. Massey previously served as a director of the Company from 1984 until 1991 when he accepted his appointment to the National Science Foundation. | |

| NICHOLAS NEGROPONTE, Principal Occupation: Chairman of the Massachusetts Institute of Technology Media Laboratory Director since 1996 Age— Mr. Negroponte is a co-founder and | |

| INDRA K. NOOYI, Principal Occupation: President and Chief Financial Officer, PepsiCo, Inc. Director since 2002 Age—47 Ms. Nooyi is President & Chief Financial Officer of PepsiCo, Inc., a world leader in convenient foods and beverages. She joined PepsiCo in 1994 as Senior Vice President of Strategic Planning, and she became Chief Financial Officer in 2000. Ms. Nooyi also serves on the Board of Directors of PepsiCo, Inc. and the PepsiCo Foundation. She serves as Successor Fellow at Yale Corporation and is on the Advisory Board of Yale University President's Council of International Activities. She is a member of the Board of the International Rescue Committee and Lincoln Center for the Performing Arts in New York City. Ms. Nooyi graduated from Madras Christian College in India with a degree in Chemistry, Physics and Math and earned a Master's Degree in Finance and Marketing from the Indian Institute of Management in Calcutta and a Master's Degree in Public and Private management from Yale University's School of Organization and Management. | |

4 PROXY STATEMENT

| JOHN E. PEPPER, JR., Principal Occupation: Chairman of the Director since 1994 Age— Mr. Pepper is Chairman of the | |

4 PROXY STATEMENT

| SAMUEL C. SCOTT III, Principal Occupation: Chairman, President and Chief Executive Officer, Corn Products International Director since 1993 Age— Mr. Scott is Chairman, President and Chief Executive Officer of Corn Products International, a corn refining business. He was President of the Corn Refining Division of CPC International from 1995 through 1997, when CPC spun off Corn Products International as a separate corporation. Mr. Scott also serves on the Board of Directors of | |

| DOUGLAS A. WARNER III, Principal Occupation: Retired; Formerly Chairman of the Board, J.P. Morgan Chase & Co. Mr. Warner was Chairman of the Board and Co-Chairman of the Executive Committee of J.P. Morgan Chase & Co., an international commercial and investment banking firm from December 2000 until he retired in November 2001. From 1995 to 2000, he was Chairman of the Board, President, and Chief Executive Officer of J.P. Morgan & Co. He is also a director of Anheuser-Busch Companies, Inc. and General Electric Co. He is on the Board of Counselors of the Bechtel Group Inc. and is a member of The Business Council. He is chairman of the Board of Managers and the Board of Overseers of Memorial Sloan-Kettering Cancer Center. Mr. Warner is a trustee of the Pierpont Morgan Library and a member of the Yale Investment Committee. Mr. Warner received a B.A. degree from Yale University. | |

| B. KENNETH WEST, Principal Occupation: Senior Consultant for Corporate Governance to Teachers Insurance and Annuity Association—College Retirement Equities Fund Director since 1976 Age— Mr. West is serving as Senior Consultant for Corporate Governance to TIAA-CREF, a major pension fund company. He retired as chairman of Harris Bankcorp, Inc. in 1995 where he had been employed since 1957. He is also a director of The Pepper Companies, Inc. and chairman of the board of the National Association of Corporate Directors (NACD). Mr. West graduated from the University of Illinois and received an MBA degree from the University of Chicago. | |

| DR. JOHN A. WHITE, Principal Occupation: Chancellor, University of Arkansas Director since 1995 Age— Dr. White is currently Chancellor of the University of Arkansas. Dr. White served as Dean of Engineering at Georgia Institute of Technology from 1991 to early 1997, having been a member of the faculty since 1975. He is also a director of Eastman Chemical Company, J.B. Hunt Transport Services, Inc., Logility, Inc., and Russell Corporation. Dr. White received a B.S.I.E. from the University of Arkansas, a M.S.I.E. from Virginia Polytechnic Institute and State University and a Ph.D. from The Ohio State University. | |

| MIKE S. ZAFIROVSKI, Principal Occupation: President and Chief Operating Officer, Motorola, Inc. Director since 2002 Age—49 Mr. Zafirovski joined Motorola in June 2000 and served as Executive Vice President and President of the Personal Communications Sector until July 25, 2002 when he was elected President and Chief Operating Officer. Prior to joining Motorola, Mr. Zafirovski spent 24 years with General Electric Company, where he served as President and CEO of GE Lighting, General Electric Company from July 1999 to May 2000 and as President and CEO of GE Lighting, Europe, Middle East and Africa, General Electric Company from April 1996 to June 1999. Mr. Zafirovski received a Bachelor of Science degree in mathematics from Edinboro University and serves on the board of directors of United Way of Lake County Illinois and Children's Memorial Hospital in Chicago. | |

PROXY STATEMENT 5

MEETINGS OF THE BOARD OF DIRECTORS OF

THE COMPANY

The Board of Directors is responsible for supervision of the overall affairs of the Company. The Board of Directors held 1214 meetings during 2001.2002. Overall attendance at Board and committee meetings was 91%93%. All directors attended 75% or more of the combined total meetings of the Board and the committees on which they served during 2001.2002, with the exception of Ms. Nooyi, who became a director on November 1, 2002 and attended 2 of 3 meetings during the remainder of 2002. The non-employee members of the Board also met in executive session without management 3 times in 2002.

Following the Annual Meeting, the Board will consist of 13 directors. In the interim between Annual Meetings, the Board has the authority under the By-laws to increase or decrease the size of the Board and fill vacancies.

CORPORATE GOVERNANCE INITIATIVES

The Board has long adhered to governance principles designed to assure the continued vitality of the Board and excellence in the execution of its duties. The Board has responsibility for management oversight and providing strategic guidance to the Company. In order to do that effectively, the Board believes it should be comprised of individuals with appropriate skills and experiences to contribute effectively to this dynamic process. The Board is currently highly diversified; it is comprised of active and former CEOs and CFOs of major corporations and individuals with experience in high-tech fields, government and academia. The Board also believes that it must continue to renew itself to ensure that its members understand the industries and the markets in which the Company operates.

As part of its renewal process, the Board previously committed to devote entire meetings to reviewing the Company's short-term and long-term strategies. The Board met this commitment and devoted a great deal of time to reviewing the Company's strategy during 2001. That focus will continue in 2002. In addition to reviewing the Company's strategy, the Board also followed-up with each significant business during the year to ensure that the business was meeting its commitments or adjusting those strategies to respond to the dynamic market conditions during the year.

The Board also adopted an improved Director Assessmentbelieves that it must be informed about the positive and Review Program. A key element of that Program is that everynegative issues, problems and challenges facing Motorola and its industries and markets so the members can exercise their fiduciary responsibilities to shareholders.

Over the last five years, beginningthe Chairman of the Board and Chief Executive Officer of Motorola, Christopher Galvin, has twice introduced renewal efforts to improve board governance. In response, the Board of Directors formed Ad Hoc Committees in February 2000 and January 2002 to drive this renewal. The members of these committees were John Pepper, past chairman and chief executive officer of Procter & Gamble who chaired the committee, Ken West, past chairman and chief executive officer of Harris Bank Corp. and now Senior Consultant for Corporate Governance at TIAA-CREF, and Christopher Galvin.

The 2002 Ad Hoc Committee on Governance devoted considerable time to further improving Motorola's governance, building on the work of the 2000 Ad Hoc Committee. The 2002 Ad Hoc Committee on Governance considered all aspects of how the board functions, including: meeting effectiveness; director involvement, development and retention; committee governance, effectiveness and composition; board and committee assessment; director assessment and review; board size, composition and independence; executive sessions; and calendar and attendance.

Some of the highlights of the Board's enhanced governance include:

These are just some of the Program, including overallhighlights of the Board's robust governance. The Board assessmentis committed to governance renewal and committee assessment, were also completed during the year.Governance and Nominating Committee will continue to build on the work of the 2000 Ad Hoc

6 PROXY STATEMENT

Committee and the 2002 Ad Hoc Committee on Governance to ensure that Motorola remains at the forefront of governance.

COMMITTEES OF THE BOARD OF DIRECTORS

To assist it in carrying out its duties, the Board has delegated certain authority to several committees. The Board currently has 76 standing committees. TheAs a result of the work of the 2002 Ad Hoc Committe on Governance described above, on February 4, 2003, the Board hasmade a number of changes in committee composition and membership. This included changing the names of certain committees and combining the former Compensation Committee and Management Development Committee into a single, new committee, the Compensation and Leadership Committee.

On February 4, 2003, the Board determined the anticipated membership of each committee for the upcoming year. Accordingly, included in the brief summaries below is the membership of each committee during the past yearat December 31, 2002 and the anticipated membership for the upcoming year.

Audit and Legal Committee

Members during 2001:at 12/31/02: Directors Jones (Chair) (not standing), Fuller, Lewent and White

Anticipated Members for Next Year: Directors Jones (Chair)Fuller (Chair since 1/1/03), Fuller, LewentWest and White

Number of Meetings in 2001: Four2002: Seven

Functions:

Compensation and Leadership Committee (combination of former Compensation Committee and former Management Development Committee)

Members during 2001: Directors Scott (Chair), Fuller and PepperAnticipated Members for Next Year:of Compensation Committee at 12/31/02: Directors Scott (Chair), Fuller and Pepper

Number of Meetings in 2001: Sevenof Compensation Committee during 2002: Six

Members of Management Development Committee at 12/31/02: Directors West (Chair), Galvin and Scott

Number of Meetings of Management Development Committee during 2002: Four

Anticipated Members of the Compensation and Leadership Committee for Next Year: Directors Scott (Chair), Nooyi, Warner and West

Functions:

Executive Committee

Members during 2001:at 12/31/02: Directors Galvin (Chair), Fuller, Growney (not standing), Lewent, Pepper, Scott, West and WestZafirovski

Anticipated Members for Next Year: Directors Galvin (Chair), Breen, Fuller, Lewent, Pepper, Scott, West and WestZafirovski

Number of Meetings in 2001:2002: None

6 PROXY STATEMENT

Finance Committee

Members during 2001:at 12/31/02: Directors Lewent (Chair), Chan (not standing), Growney (not standing)Caio, Warner, West and WestZafirovski

Anticipated Members for Next Year: Directors Lewent (Chair), Breen, Caio, Warner and WestZafirovski

Number of Meetings in 2001: Four2002: Five

Functions:

Management Development PROXY STATEMENT 7

Governance and Nominating Committee (formerly known as Nominating Committee)

Members during 2001: Directors West (Chair), Galvin and ScottAnticipated Members for Next Year: Directors West (Chair), Galvin and ScottNumber of Meetings in 2001: FourFunctions:

Nominating Committee

Members during 2001:at 12/31/02: Directors Pepper (Chair), ChanJones (not standing), Jones, Massey, Negroponte and NegroponteWarner

Anticipated Members for Next Year: Directors Pepper (Chair), Jones, Massey, Negroponte and WarnerNooyi

Number of Meetings in 2001: Three2002: Two

Functions:

This Committee will consider a candidate for director proposed by a stockholder. A candidate must be highly qualified and be both willing and expressly interested in serving on the Board. A stockholder wishing to propose a candidate for the Committee's consideration should forward the candidate's name and information about the candidate's qualifications to the Company's Secretary as described on page 30.31.

Technology and Design Committee (formerly known as Technology Committee)

Members during 2001:at 12/31/02: Directors Massey (Chair), Caio, Growney (not standing), Negroponte, White and WhiteZafirovski

Anticipated Members for Next Year: Directors Massey (Chair), Breen, Caio, NegroponteGalvin and WhiteNegroponte

Number of Meetings in 2001:2002: Four

Functions:

DIRECTOR COMPENSATION AND RELATED TRANSACTIONS

Directors who are also employees of Motorola receive no additional compensation for serving on the Board or its committees.

For each non-employee director,During 2002, the annual retainer fee is $60,000 andpaid to each non-employee director was $60,000. In addition, each non-employee director who isserved as a chair of a committee receivesreceived an additional $4,000 per year.annual fee. The Company also reimburses its directors, and in certain instancescircumstances spouses who accompany directors, for travel, lodging and related expenses they incur in attending Board and committee meetings.

On May 7, 2002, each non-employee director received options to acquire 15,000 shares of Common Stock at the fair market value of the shares on the date of grant.

The fees paid to the Company's directors have not changed since 2000. After reviewing the fees paid to directors of other companies in the Company's peer group and recognizing the ever-increasing demands on directors of public companies, the Board revised its compensation program, effective January 1, 2003. In 2003, the annual retainer fee paid to each non-employee director will increase to $75,000. The non-employee director chairs of the Audit and Legal Committee and Compensation and Leadership Committee will receive an additional $12,000 annual fee. Non-employee directors who serve as chairs of other committees will receive an additional $5,000 annual fee. In addition, the members of the Audit and Legal Committee (other than the Chair) will receive an additional $5,000 annual fee. Directors are expected to continue to be granted options to purchase shares of Common Stock each year.

Directors are required to accept half of all their Board compensation in Common Stock or restricted Common Stock, and may elect to accept up to 100% of their compensation in Common Stock or restricted Common Stock. Restricted Common Stock is Common Stock that may not be transferred and is subject to repurchase by Motorola until either: (i) the holder has served as a member of the Board for at least four years and does not stand for re-election or is not re-elected, or (ii) the holder's disability or death. Non-employee directors may elect to defer receipt of all or any portion of their compensation that is not otherwise required to be paid in Common Stock or restricted Common Stock. Since 2001, non-employee directors can elect to participate in the Motorola Management Deferred Compensation Plan. This plan offers a wide variety of investment options. Directors may elect to have distributions while they are directors or after they retire from the Board.

On June 1, 2001, each non-employee director received an option to acquire 15,000 shares of Common Stock at the fair market value of the shares on the date of grant.

PROXY STATEMENT 7

In 1996, the Board terminated its retirement plan. Non-employee directors elected to the Board after the termination date are not entitled to benefits under this plan, and non-employee directors already participating in the plan accrued no additional benefits for services after May 31, 1996. In 1998, some directors converted their accrued benefits in the retirement plan into shares of restricted Common Stock. They may not sell or transfer these shares and these shares are subject to repurchase by Motorola until they are no longer members of the Board because either: (i) they did not stand for re-election or were not re-elected, or (ii) their disability or death. Directors Jones and Massey did not convert their accrued benefits in the retirement plan and are entitled to receive payment of such benefits in accordance with the applicable payment terms of the retirement plan, including payments to spouses in the event of death. For each year of service on the Board prior to the date the plan was terminated, these directors are entitled to receive annual payments equal to 10% of the annual retainer for directors

8 PROXY STATEMENT

in effect on the date the plan was terminated, with a maximum annual payment equal to 80% of the retainer. Each of these Directors had served on the Board for eight or more years prior to the termination of the plan and, accordingly, are fully vested and will be entitled to an annual payment of $32,000.$32,000 upon retirement from the Board.

Non-employee directors are covered by insurance that provides accidental death and dismemberment coverage of $500,000 per person. The spouse of each such director is also covered by such insurance when traveling with the director on business trips for the Company. The Company pays the premiums for such insurance. The total premiums for coverage of all such directors and their spouses during the year ended December 31, 20012002 was $3,500.$2,750.

Motorola has obtained investment banking and other financial services from J.P. Morgan Chase & Co. ("J.P. Morgan Chase") and certain of its subsidiaries. Mr.Director Warner served as Chairman of the Board and Co-Chairman of the Executive Committee of J.P. Morgan Chase from December 2000 until he retired in November 2001. As further described under "Legal Proceedings" in the Company's Form 10-K for the year ended December 31, 2001,2002, Motorola and The Chase Manhattan Bank ("Chase Manhattan"), a wholly-owned subsidiary of J.P. Morgan Chase, arewere involved in a number of lawsuits relating to loans extended by a group of lenders (for whom Chase Manhattan acted as agent) to Iridium LLC. The parties to these lawsuits reached a settlement in March 2003.

THE BOARD OF DIRECTORS RECOMMENDS A VOTEFOR THE ELECTION OF THE NOMINEES NAMED HEREIN AS DIRECTORS. UNLESS INDICATED OTHERWISE BY YOUR PROXY VOTE, THE SHARES WILL BE VOTEDFOR THE ELECTION AS DIRECTORS OF SUCH NOMINEES.

PROPOSAL 2

ADOPTION OF THE MOTOROLA OMNIBUS INCENTIVE PLAN OF 20022003

The Board has adopted the Motorola Omnibus Incentive Plan of 20022003 (the "2002"2003 Plan") and is recommending that stockholders approve the 20022003 Plan at the Annual Meeting. The 20022003 Plan is integral to the Company's compensation strategies and programs. The use of stock options and other stock awards among technology companies is widely prevalent. The 20022003 Plan will maintain the flexibility that Motorola needs to keep pace with its competitors and effectively recruit, motivate, and retain the caliber of employees essential for achievement of the Company's success.

The 20022003 Plan will permit stock option grants, annual management incentive awards, stock grants, restricted stock grants, restricted stock unit grants, performance stock grants, performance unit grants, stock appreciation rights grants ("SARs"), and cash awards. Stockholder approval of the 20022003 Plan will permit the performance-based awards discussed below to qualify for deductibility under Section 162(m) of the Internal Revenue Code ("Code").

Awards and grants under the 20022003 Plan are referred to as "Benefits." Those eligible for Benefits under the 20022003 Plan are referred to as "Participants." Participants include all employees of the Company and its subsidiaries and all non-employee directors of the Company.

As of December 31, 2001,2002, approximately 58.329 million shares were available for new grants under the Company's existing stock incentive plans and there were approximately 219.5280.8 million shares subject to outstanding benefits under these and predecessor plans. While the existing stock incentive plans will remain in place, they do not provide sufficient shares for market-competitive grant levels prior to the 20032004 stockholder meeting.

8 PROXY STATEMENT 9

A summary of the principal features of the 20022003 Plan is provided below, but is qualified in its entirety by reference to the full text of the 20022003 Plan that was filed electronically with this proxy statement with the Securities and Exchange Commission. Such text is not included in the printed version of this proxy statement. A copy of the 20022003 Plan is available from the Company's Secretary at the address on the cover of this document.

Shares Available for Issuance

The aggregate number of shares of Common Stock that may be issued under the 20022003 Plan will not exceed 4595 million (subject to the adjustment provisions discussed below). The 4595 million new shares represent 2.04.1 percent of the currently outstanding shares of Common Stock.

The number of shares that may be issued under the 20022003 Plan for Benefits other than stock options and SARs will not exceed a total of 540 million shares (subject to the adjustment provisions discussed below).

Administration and Eligibility

The 20022003 Plan will be administered by a Committee of the Board (the "Committee") consisting of two or more directors, each of whom will satisfy the requirements established for administrators acting under plans intended to qualify as a "non-employee director" within the meaning set forth infor exemption under Rule 16b-3 promulgated under the Securities Exchange Act of 1934 as amended (the "Exchange("Exchange Act")., for outside directors acting under plans intended to qualify for exemption under Section 162(m) of the Code and with any applicable requirements established by the New York Stock Exchange. The Committee will approve the aggregate Benefits and the individual Benefits for the most senior elected officers and non-employee directors. The Committee may delegate some of its authority under the administration of the 20022003 Plan in accordance with the terms of the 20022003 Plan.

No Participant may receive in any Plan Year:calendar year: (i) stock options relating to more than 3,000,0003 million shares; (ii) restricted stock or restricted stock units that are subject to the attainment of performance goals (as described below) relating to more than 300,0001.5 million shares; (iii) SARs relating to more than 3,000,0003 million shares; or (iv) performance shares relating to more than 300,0001.5 million shares. No non-employee director may receive in any calendar year (i) stock options relating to more than 30,000 shares (allor (ii) restricted stock units relating to more than 30,000 shares. (Each of thesethe above limits is subject to the adjustment provisions discussed below).below.) The maximum amount that may be earned under Performance Unit awards by any Participant who is a covered employee within the meaning of Section 162(m) of the Code ("Covered Employee") in any calendar year may not exceed $5,000,000.$8.5 million.

Benefits

Stock Options

Grants of Options

The Committee is authorized to grant stock options to Participants ("Optionees"), which may be either incentive stock options ("ISOs") or nonqualified stock options ("NSOs"). NSOs and ISOs are collectively referred to as "Stock Options." The exercise price of any Stock Option must be equal to or greater than the fair market value of the shares on the date of the grant. The term of a Stock Option cannot exceed 10 years. ISOs may not be granted more than 10 years after the date that the 20022003 Plan was adopted by the Board.

For purposes of the 20022003 Plan, fair market value shall be determined in such manner as the Committee may deem equitable, or as required by applicable law or regulation. Generally, fair market value means the closing price on the last trading day preceding the day of the transaction, as reported for the New York Stock Exchange Composite Transactions in the Wall Street Journal.

Exercisability and Termination

At the time of grant, the Committee in its sole discretion will determine when Options are exercisable and when they expire.

Payment of Option Price

Payment for shares purchased upon exercise of a Stock Option must be made in full at the time of purchase. Payment may be made in cash, by the transfer to the Company of shares owned by the Participant for(held at least six months (valued atif the Company is accounting for Stock Options using APB Opinion 25 or purchased on the open market) having a fair market value on the date of transfer) or atransfer equal to the option exercise price (or certification of ownership of such sharesshares) or in such other manner as may be authorized by the Committee.

SARs

The Committee has the authority to grant SARs to Participants and to determine the number of shares subject to each SAR, the term of the SAR, the time or times at which the SAR may be exercised, and all other terms and conditions of the SAR. A SAR is a right, denominated in shares, to receive, upon exercise of the right, in whole or in part, without payment to the Company an amount, payable in shares, in cash or a combination thereof, that is equal to the excess of: (i) the fair market value of Common Stock on the date of exercise of the right; over (ii) the fair market value of Common Stock on the date of grant of the right multiplied by the number of shares for which the right is exercised. The Committee also may, in its discretion, substitute SARs which can be settled only in Common Stock for outstanding Stock Options at any time when the Company is subject to fair value accounting. The terms and conditions of any substitute SAR shall be substantially the same as those applicable to the Stock Option that it replaces and the term of the substitute SAR shall not exceed the term of the Stock Option that it replaces.

Restricted Stock and Restricted Stock Units

Restricted Stock consists of shares which are transferred or sold by the Company to a Participant, but are subject to substantial risk of forfeiture and to restrictions on their sale or other transfer by the Participant. Restricted Stock Units are the right to receive shares at a future date in accordance

10 PROXY STATEMENT

with the terms of such grant upon the attainment of certain conditions specified by the Committee.Committee which include substantial risk of forfeiture and restrictions on their sale or other transfer by the Participant. The Committee determines the eligible Participants to whom, and the time or times at which, grants of Restricted Stock or Restricted Stock Units will be made, the number of shares or units to be granted, the price to be paid, if any, the time or times within which the shares covered by such grants will be subject to forfeiture, the time or times at which the restrictions will terminate, and all other terms and conditions of the grants. Restrictions or conditions could include, but are not limited to, the attainment of performance goals (as described below), continuous service with the Company, the passage of time or other restrictions or conditions. Generally, the Restricted Stock and Restricted Stock Units that are currently outstanding vest between three to five years after the date of grant.

Performance Stock

A Participant who is granted Performance Stock has the right to receive shares or cash or a combination of shares and cash equal to the fair market value of such shares at a future date in accordance with the terms of such grant and upon the attainment of performance goals specified by the Committee.

The award of Performance Stock to a Participant will not create any rights in such Participant as a stockholder of the Company until the issuance of Common Stock with respect to an award.

PROXY STATEMENT 9

Performance Units

A Participant who is granted Performance Units has the right to receive a payment in cash upon the attainment of performance goals.goals specified by the Commitee. The Committee may substitute actual shares of Common Stock for the cash payment otherwise required to be made pursuant to a Performance Unit award.

Performance Goals

Awards of Restricted Stock, Restricted Stock Units, Performance Stock, Performance Units and other incentives under the 20022003 Plan may be made subject to the attainment of performance goals relating to one or more business criteria within the meaning of Section 162(m) of the Code, including, but not limited to: cash flow; cost; ratio of debt to debt plus equity; profit before tax; economic profit; earnings before interest and taxes; earnings before interest, taxes, depreciation and amortization; earnings per share; operating earnings; economic value added; ratio of operating earnings to capital spending; free cash flow; net profit; net sales; sales growth; price of the Common Stock; return on net assets, equity, or stockholders' equity; market share; or total return to stockholders ("Performance Criteria").

Any Performance Criteria may be used to measure the performance of the Company as a whole or any business unit of the Company and anymay be measured relative to a peer group or index. Any Performance Criteria may be adjusted to include or exclude extraordinary items.

SARs

The Committee hasspecial items as identified in the authority to grant SARs to Participants and to determine the number of shares subject to each SAR, the term of the SAR, the timeCompany's quarterly or times at which the SAR may be exercised, and all other terms and conditions of the SAR. An SAR is a right, denominated in shares, to receive, upon exercise of the right, in whole or in part, without payment to the Company an amount, payable in shares, in cash or a combination thereof, that is equal to the excess of: (i) the fair market value of Common Stock on the date of exercise of the right; over (ii) the fair market value of Common Stock on the date of grant of the right multiplied by the number of shares for which the right is exercised. It is anticipated that SARs primarily will be used in place of stock options, and any appreciation in value will be paid in cash, in order to comply with the laws and regulations of foreign jurisdictions or to make the grant a more effective form of compensation in a foreign jurisdiction.annual earnings releases.

Annual Management Incentive Awards

The Committee has the authority to grant Management Incentive Awards to designated executive officers of the Company or any subsidiary.

Management Incentive Awards will be paid out of an incentive pool equal to 5 percent of the Company's consolidated operating earnings for each calendar year. The Committee will allocate an incentive pool percentage to each designated Participant for each calendar year. In no event, may the incentive pool percentage for any one Participant exceed 30 percent of the total pool. For purposes of the 20022003 Plan, "consolidated operating earnings" will mean the consolidated earnings before income taxes of the Company, computed in accordance with generally accepted accounting principles, but shall exclude the effects of extraordinaryspecial items. ExtraordinarySpecial items mean:include: (i) extraordinary, unusual, and/or nonrecurring items of gain or loss;loss, (ii) gains or losses on the disposition of a business;business, (iii) changes in tax or accounting regulations or laws;laws, or (iv) the effect of a merger or acquisition.acquisition, all as identified in the Company's quarterly and annual earnings releases. The Participant's incentive award then will be determined by the Committee based on the Participant's allocated portion of the incentive pool subject to adjustment in the sole discretion of the Committee. In no event may the portion of the incentive pool allocated to a Participant who is a Covered Employee be increased in any way, including as a result of the reduction of any other Participant's allocated portion.

Stock Awards

The Committee may award shares of Common Stock to Participants without payment therefore, as additional compensation for service to the Company or a subsidiary. Stock awards may be subject to other terms and conditions, which may vary from time to time and among employees, as the Committee determines to be appropriate.

Cash Awards

A cash award consists of a monetary payment made by the Company to an employee as additional compensation for his or her services to the Company or a subsidiary. A cash award may be made in tandem with another Benefit or may be made independently of any other Benefit. Cash awards may be subject to other terms and conditions, which may vary from time to time and among employees, as the Committee determines to be appropriate.

Amendment of the 20022003 Plan

The Board or the Committee has the right and power to amend the 20022003 Plan, provided, however, that neither the Board nor the Committee may amend the 20022003 Plan in a manner which would impair or adversely affect the rights of the holder of a Benefit without the holder's consent. IfNo material amendment of the Code or any other applicable statute, rule or regulation, including, but not limited to, those of any securities exchange, requiresPlan shall be made without stockholder approval with respect to the 2002 Plan or any type of amendment thereto, then to the extent so required, stockholder approval will be obtained.approval.

PROXY STATEMENT 11

Termination of the 20022003 Plan

The Board may terminate the 20022003 Plan at any time. Termination will not in any manner impair or adversely affect any Benefit outstanding at the time of termination.

Committee's Right to Modify Benefits

Any Benefit granted may be converted, modified, forfeited, or canceled, in whole or in part, by the Committee if

10 PROXY STATEMENT

and to the extent permitted in the 2002 Plan, or applicable agreement entered into in connection with a Benefit grant or with the consent of the Participant to whom such Benefit was granted. The Committee may grant Benefits on terms and conditions different than those specified in the 20022003 Plan to comply with the laws and regulations of any foreign jurisdiction, or to make the Benefits more effective under such laws and regulations.

The Committee may permit or require a Participant to have amounts or shares of Common Stock that otherwise would be paid or delivered to the Participant as a result of the exercise or settlement of an award under the 2003 Plan credited to a deferred compensation or stock unit account established for the Participant by the Committee on the Company's books of account.

Neither the Board nor the Committee may cancel any outstanding Stock Option for the purpose of reissuing the option to the Participant at a lower exercise price, or to reduce the option price of an outstanding option.

Change in Control

Stock Options

Upon the occurrence of a Change in Control, each Stock Option outstanding on the date on which the Change in Control occurs will immediately become exercisable in full.

Restricted Stock and Restricted Stock Units

Upon the occurrence of a Change in Control, the restrictions on all shares of Restricted Stock and Restricted Stock Units outstanding on the date on which the Change in Control occurs will be automatically terminated. With regard to Restricted Stock Units, shares of Common Stock will be delivered to the Participant in the amount or amounts as determined in accordance with the terms and conditions in the applicable agreement relating to Restricted Stock Units.

Performance Stock

Upon the occurrence of a Change in Control, any performance goal with respect to any outstanding Performance Stock will be deemed to have been attained at target levels, and shares of Common Stock or cash will be paid to the Participant in an amount or amountsas determined in accordance with the terms and conditions set forth in the applicable agreement relating to the Performance Stock.

Performance Units

Upon the occurrence of a Change in Control, any performance goal with respect to any outstanding Performance Units will be deemed to have been attained at target levels, and the cash (or shares of Common Stock) will be paid to the Participant in an amount or amountsas determined in accordance with the terms and conditions set forth in the applicable agreement relating to the Performance Units.

SARs

Upon the occurrence of a Change in Control, each SAR outstanding on the date on which the Change in Control occurs will immediately become exercisable in full.

Management Incentive Awards

Upon the occurrence of a Change in Control, all Management Incentive Awards will be paid out based on the consolidated operating earnings of the immediately preceding year, or such other method of payment as may be determined by the Committee (prior to the Change in Control).

Other Stock or Cash Awards

Upon the occurrence of a Change in Control, any terms and conditions with respect to other stock or cash awards previously granted under the 20022003 Plan will be deemed to be fully satisfied and the other stock or cash awards will be paid out immediately to the Participants, in amountsas determined in accordance with the terms and conditions set forth in the applicable grant, award, or agreement relating to such Benefits.

For purposes of the 20022003 Plan, the term "Change in Control" is defined as: (i) any change in the person or group that possesses, directly or indirectly, the power to direct or cause the direction of the management and the policies of the Company, whether through the ownership of voting securities, by contract or otherwise; (ii) the acquisition, directly or indirectly, of securities of the Company representing at least 20 percent of the combined voting power of the outstanding securities of the Company (other than by the Company, or any employee benefit plan of the Company); (iii) the consummation of certain mergers and consolidations involving the Company; (iv) the consummation of the sale or other disposition of all or substantially all of the Company's assets; (v) athe approval of liquidation or dissolution of the Company approved by its stockholders; and (vi) a change in the majority of the Board of the Company in existence prior to the first public announcement relating to any cash tender offer, exchange offer, merger or other business combination, sale of assets, proxy or consent solicitation (other than by the Board of the Company), contested election or substantial stock accumulation.

Adjustments

If there is any change in the Common Stock by reason of any stock split, stock dividend, spin-off, split-up, spin-out, recapitalization, merger, consolidation, reorganization, combination, or exchange of shares, the total number of shares available for Benefits, the maximum number of

12 PROXY STATEMENT

shares which may be subject to an award in any calendar year and the number of shares subject to outstanding Benefits, and the price of each of the foregoing, as applicable, will be equitably adjusted by the Committee in its discretion.

Subject to the Change-in-Control provisions, without affecting the number of shares reserved or available hereunder, either the Board or the Committee may authorize the issuance or assumption of Benefits in connection with any merger, consolidation, acquisition of property or stock, or reorganization upon such terms and conditions as it deems appropriate.

PROXY STATEMENT 11

In the event of any merger, consolidation, or reorganization in whichof the Company is notwith or into another corporation which results in the continuing corporation,Company's outstanding Common Stock being converted into or exchanged for different securities, cash, or other property, there shall be substituted on an equitable basis as determined by the Committee, for each share of common stockCommon Stock subject to a Benefit, the number and kind of shares of stock, other securities, cash, or other property to which holders of Common Stock of the Company are entitled pursuant to the transaction.

Substitution and Assumption of Benefits

Without affecting the number of shares reserved or available under the 2003 Plan, either the Board or the Committee may authorize the issuance of Benefits in connection with the assumption of, or substitution for, outstanding benefits previously granted to individuals who become employees of the Company or any subsidiary as the result of any merger, consolidation, acquisition of property or stock, or reorganization other than a Change in Control, upon such terms and conditions as it deems appropriate.

Reusage

If a Stock Option granted under the 20022003 Plan expires or is terminated, surrendered or canceled without having been fully exercised or if Restricted Stock, Restricted Stock Units, Performance Shares or SARs granted under the 20022003 Plan are forfeited or terminated without the issuance of all of the shares subject thereto, the shares covered by such Benefits will again be available for use under the 20022003 Plan. Shares covered by a Benefit granted under the 20022003 Plan would not be counted as used unless and until they are actually issued and delivered to a Participant. Any shares of Common Stock covered by a SAR shall be counted as used only to the extent shares are actually issued to the Participant upon exercise of the SAR. The number of shares which are transferred to the Company by a Participant to pay the exercise or purchase price of a Benefit will be subtracted from the number of shares issued with respect to such Benefit for the purpose of counting shares used. Shares withheld to pay withholding taxes in connection with the exercise or payment of a Benefit will not be counted as used. Shares covered by a Benefit granted under the 20022003 Plan that is settled in cash will not be counted as used.

Federal Income Tax Consequences

The Company has been advised by counsel that the federal income tax consequences as they relate to Benefits are as follows:

ISOs

An Optionee does not generally recognize taxable income upon the grant or upon the exercise of an ISO. Upon the sale of ISO shares, the Optionee recognizes income in an amount equal to the difference, if any, between the exercise price of the ISO shares and the fair market value of those shares on the date of sale. The income is taxed at long-term capital gains rates if the Optionee has not disposed of the stock within two years after the date of the grant of the ISO and has held the shares for at least one year after the date of exercise and the Company is not entitled to a federal income tax deduction. The holding period requirements are waived when an Optionee dies.

The exercise of an ISO may in some cases trigger liability for the alternative minimum tax.

If an Optionee sells ISO shares before having held them for at least one year after the date of exercise and two years after the date of grant, the Optionee recognizes ordinary income to the extent of the lesser of: (i) the gain realized upon the sale; or (ii) the difference between the exercise price and the fair market value of the shares on the date of exercise. Any additional gain is treated as long-term or short-term capital gain depending upon how long the Optionee has held the ISO shares prior to disposition. In the year of disposition, the Company receives a federal income tax deduction in an amount equal to the ordinary income whichthat the Optionee recognizes as a result of the disposition.

NSOs

An Optionee does not recognize taxable income upon the grant of an NSO. Upon the exercise of such a Stock Option, the Optionee recognizes ordinary income to the extent the fair market value of the shares received upon exercise of the NSO on the date of exercise exceeds the exercise price. The Company receives an income tax deduction in an amount equal to the ordinary income that the Optionee recognizes upon the exercise of the Stock Option.

Restricted Stock

A Participant who receives an award of Restricted Stock does not generally recognize taxable income at the time of the award. Instead, the Participant recognizes ordinary income in the first taxable year in which his or her interest in the shares becomes either: (i) freely transferable; or (ii) no longer subject to substantial risk of forfeiture. The amount of taxable income is equal to the fair market value of the shares less the cash, if any, paid for the shares.

A Participant may elect to recognize income at the time he or she receives Restricted Stock in an amount equal to

PROXY STATEMENT 13

the fair market value of the Restricted Stock (less any cash paid for the shares) on the date of the award.

The Company receives a compensation expense deduction in an amount equal to the ordinary income recognized by the Participant in the taxable year in which restrictions lapse (or in the taxable year of the award if, at that time, the Participant had filed a timely election to accelerate recognition of income).

Other Benefits

In the case of an exercise of an SAR or an award of Restricted Stock Units, Performance Stock, Performance Units, or Common Stock or cash, the Participant will generally recognize ordinary income in an amount equal to any cash received and the fair market value of any shares received on the date of payment or delivery. In that taxable year, the Company will receive a federal income tax deduction in an amount equal to the ordinary income which the Participant has recognized.

Million Dollar Deduction Limit

The Company may not deduct compensation of more than $1,000,000 that is paid to an individual who, on the last day of the taxable year, is either the Company's chief executive officer or is among one of the four other most highly-compensated officers for that taxable year.year as reported in the Company's proxy statement. The limitation on deductions does not apply to certain types of compensation, including qualified performance-based compensation. The Company believes that Benefits in the form of

12 PROXY STATEMENT

Stock Options, Performance Stock, Performance Units, SARs, performance-based Restricted Stock and Restricted Stock Units and cash payments under Management Incentive Awards constitute qualified performance-based compensation and, as such, will be exempt from the $1,000,000 limitation on deductible compensation.

Miscellaneous

A new benefits table is not provided because no grants have been made under the 20022003 Plan and all Benefits are discretionary. On March 15, 2002,14, 2003, the closing price of the Common Stock was $14.00.$8.19.

Approval by Stockholders

In order to be adopted, the 20022003 Plan must be approved by the affirmative vote of a majority of the outstanding shares represented at the meeting and entitled to vote.

RECOMMENDATION OF THE BOARD

THE BOARD OF DIRECTORS RECOMMENDS A VOTEFOR ADOPTION OF THE MOTOROLA OMNIBUS INCENTIVE PLAN OF 2002.2003. UNLESS OTHERWISE INDICATED ON THE PROXY, THE SHARES WILL BE VOTEDFOR ADOPTION OF THE MOTOROLA OMNIBUS INCENTIVE PLAN OF 2002.2003.

14 PROXY STATEMENT

PROPOSAL 3AMENDMENT TO THE MOTOROLA EMPLOYEE STOCK PURCHASEEQUITY COMPENSATION PLAN OF 1999

INFORMATION

The Boardfollowing table summarizes the Company's equity compensation plan information as of Directors believes itDecember 31, 2002. The table does not include information with respect to options assumed in acquisitions where the plans governing the options will not be used for future awards, as described below. The table also does not include information about the proposed 2003 Plan that is inbeing submitted for stockholder approval at the best interests ofannual meeting. No grants have been made under the Company2003 Plan.

| Plan Category | Number of securities to be issued upon exercise of outstanding options and rights (a) | Weighted-average exercise price of outstanding options and rights (b) | Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) (c) | |||||

|---|---|---|---|---|---|---|---|---|

| Equity Compensation plans approved by Motorola stockholders | 266,737,438 | (1)(2)(3) | $ | 20.40 | 92,090,191 | (4) | ||

| Equity compensation plans not approved by Motorola stockholders(5)(6) | 14,080,774 | (7) | $ | 16.98 | 877,860 | (8) | ||

| Total | 280,818,212 | $ | 20.23 | 92,968,051 | ||||

If our shareholders approve this amendment, an additional 50 million shares will be available for purchase by eligible employees under the Employee Purchase Plan. As of March 15, 2002, the Company had issued and employees had purchased 24,013,592 shares of the original 54.3 million shares authorized under the Employee Purchase Plan. The Company estimates that an additional 8.5 million shares will be issued and purchased for the six-month purchase period ending March 29, 2002. Accordingly, there is the possibility that, without this amendment, there would be insufficient authorized shares for all issuances before the 2003 Annual Meeting. The Company believes that the additional authorized shares will be sufficient for purchases under the plan for approximately three more years.

A summary of the principal features of the Employee Purchase Plan as administered in the U.S. is provided below, but is qualified in its entirety by reference to the full text of the Employee Purchase Plan that was filed electronically with this proxy statement with the Securities and Exchange Commission. Such text is not included in the printed version of this proxy statement. A copy of the Employee Purchase Plan is available from the Company's Secretary at the address on the cover of this document. A copy of the Employee Purchase Plan is available from the Company's Secretary at the address on the cover of this document.

Administration and Eligibility

The Employee Purchase Plan is administered by the Compensation Committee of the Board of Directors (the "Committee"). The Committee has the authority to make rules and regulations governing the administration of the Employee Purchase Plan. The Committee may delegate the administration of the Employee Purchase Plan in accordance with the terms of the plan.

Substantially all full-time employees of the Company and designated subsidiaries are eligible to participate in the Employee Purchase Plan, except that the following may be excluded at the discretion of the Committee: (i) employees whose customary employment is 20 hours or less per week; and (ii) employees whose customary employment is for not more than 5 months per year. As of December 31, 2001, approximately 100,000 employees were eligible to participate in the Employee Purchase2000 Plan and approximately 44,000 employees participate in the Employee Purchase2002 Plan.

Participation and Terms

An eligible employee may elect to participate in the Employee Purchase Plan as of any Enrollment Date. "Enrollment Dates" occur on the first day of the offering period which is currently set at six-month intervals beginning on approximately April 1 and October 1. To participate in the Employee Purchase Plan an employee must complete an enrollment and payroll deduction authorization form provided by the Company which indicates the amounts to be deducted from his or her salary and applied to the purchase of the shares on the Share Purchase Date (as hereinafter defined). The payroll deduction must be within limits set by the Committee.

A payroll deduction account is established for each participating employee by the Company and all payroll deductions made on behalf of each employee are credited to each such employee's respective payroll deduction account. On the last trading day of each offering period (the "Share Purchase Date"), the amount credited to each participating employee's payroll deduction account is applied to purchase as many shares as may be purchased with such amount at the applicable purchase price.

The purchase price for the Shares will not be less than the lesser of 85% of the closing price of shares of Common

PROXY STATEMENT 13

Stock as reported on the New York Stock Exchange (i) on the first trading day of the applicable offering period or (ii) on the Share Purchase Date. Employees may purchase shares through the Employee Purchase Plan only by payroll deductions.

Amendment and Termination

The Board of Directors of the Company may amend the Employee Purchase Plan at any time, provided that if stockholder approval is required for the plan to continue to comply with the requirements of Securities and Exchange Commission Regulation Section 240.16b-3 or Section 423 of the Internal Revenue Code (the "Code"), such amendment shall not be effective unless approved by the Company's stockholders within twelve months after the date of the adoption by the Board of Directors.

The Employee Purchase Plan may be terminated by the Board of Directors at any time.

Federal Income Tax Consequences

The Employee Purchase Plan Each restricted stock unit is intended to be an "employeethe economic equivalent of a share of Common Stock.

If the participant sells or otherwise disposes of the shares within that two-year period, the participant will recognize ordinary income at the time of dispositioneach SAR granted, cash in an amount equal to the excess of the fair market pricevalue of the shares on the date of purchase over the purchase price and the Company will be entitled to a tax deduction for the same amount.

If the participant sells or otherwise disposes of the shares after holding the shares for the two-year period, the participant will recognize ordinary income at the time in an amount equal to the lesser of (i) the excess of the market price of the shares on the first day of the offering period over the purchase price, or (ii) the excess of the market price of the shares at the time of disposition over the purchase price. The Company will not be entitled to any tax deduction with respect to shares purchased under the Employee Purchase Plan if the shares are held for the requisite two-year period.

The employee may also recognize capital gain or loss at the time of disposition of the shares, either short-term or long-term, depending on the holding period for the shares.

Other Information

On March 15, 2002, the closing priceone share of the Common Stock on the date the SAR is exercised over the fair market value of one share of Common Stock on the date the SAR was $14.00.

RECOMMENDATION OF THE BOARD

THE BOARD OF DIRECTORS RECOMMENDS granted. No security is issued upon the exercise of these SARs.

PROPOSAL 4SHAREHOLDER PROPOSAL RE: NON-AUDIT SERVICES BY INDEPENDENT AUDITORS

For reasons stated below, the Board of DirectorsPlan") that was adopted in November 2000. One of the Company recommends a vote "AGAINST" this shareholder proposal.

The Company has been advised that the Sheet Metal Workers' National Pension Fund, 601 North Fairfax Street, Suite 500, Alexandria, Virginia 22314-2075, the beneficial owner of 162,000 shares, intends to submit the following proposal for consideration at the 2002 annual meeting:

RESOLVED, that the shareholders of Motorola, Inc. ("Company") request that the Board of Directors adopt a policy stating that the public accounting firm retained by our Company to provide audit services, or any affiliated company, should not also be retained to provide non-audit services to our Company.

Statement of Support: The role of independent auditors in ensuring the integritymajor purposes of the financial statementsC/A Plan is to grant awards to persons newly hired by the Company, including persons becoming employees as a result of public corporations is fundamentally importantan acquisition transaction; otherwise grants are generally made by the Company under the 1998, 2000 and 2002 Plans noted in footnote 1 above. Awards may not be made under the C/A Plan to the efficient and effective operationdirectors or executive officers of the financial markets.Company. The U.S. Securities and Exchange Commission recently stated:

Independent auditors have an important public trust. Investors must be ableC/A Plan is more fully described below.

It is critically important to the integrity of the auditing process and the confidence of investors that those firms performing audits for public corporations avoid business relationships that might compromise their independence or raise the perception of compromised judgment. At the heart of the challenge to auditor independence is the growing level of business and financial relationships developing between audit firms and their clients. Bulletin #14 identifies these growing business relationships that threaten auditor independence:

Accounting firms have woven an increasingly complex web of business and financial relationships with their

14 PROXY STATEMENT

audit clients. The nature of the non-audit services that accounting firms provide to their audit clients has changed, and the revenues from these services have dramatically increased.

The growth of non-audit revenues represents a trend that has been accelerating dramatically in the last several years, with non-audit fees for consulting or advisory services exceeding audit fees at many companies. Our Company is in the category of companies that pays its audit firm more for non-audit advisory services than it does for audit services. The Company's most recent proxy statement indicated that for fiscal year 2000 KPMG LLP billed $3.9 million for audit services rendered, while it billed $62.3 million for non-audit services rendered.

We believe that this financial "web of business and financial relationships" may at a minimum create the perception of a conflict of interest that could result in a lack of owner and investor confidence in the integrity of the Company's financial statements. As long-term shareowners, we believe that the best means of addressing this issue is to prohibit any audit firm retained by our Company to perform audit services from receiving payment for any non-audit services performed by the firm.